Understanding the option Greeks

Delta, gamma, theta, vega and rho — the metrics that measure how an option's price reacts to the market.

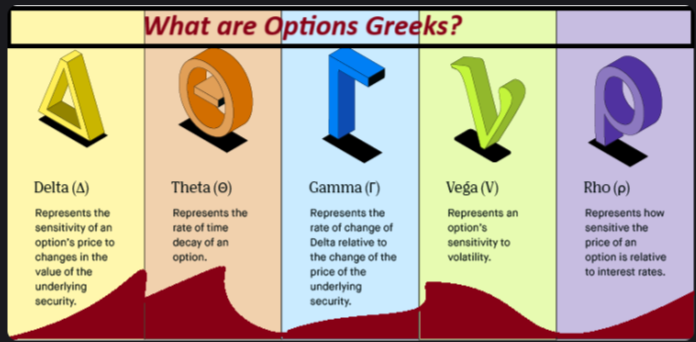

What are the Greeks?

The Greeks are metrics that measure how sensitive an option's price — its premium — is to different forces: the underlying price, time, volatility and interest rates. Master them and you can manage risk and trade with intent instead of guessing.

Delta (Δ) — price sensitivity

Delta measures how much an option's price moves for every $1 move in the underlying.

Calls run from 0 to +1; puts from 0 to −1.

Example: a call with a 0.50 Delta gains about $0.50 if the stock rises $1.

Higher Delta means more sensitivity to the underlying. Delta also roughly estimates the chance the option expires in-the-money.

Gamma (Γ) — how fast Delta moves

Gamma is the rate of change of Delta as the underlying moves. It's highest at-the-money and falls as the option goes deep in- or out-of-the-money.

Example: a call with 0.50 Delta and 0.05 Gamma — a $1 rise pushes Delta from 0.50 to 0.55.

Gamma tells you how stable Delta is. High-Gamma options are riskier for short-term trading.

Theta (Θ) — time decay

Theta is how fast an option's extrinsic value bleeds away as time passes. It's negative for all options, and it accelerates as expiration approaches.

Example: a Theta of −0.10 means the option loses about $0.10 a day, even if the stock doesn't move.

Short-dated options decay fastest. Sellers (e.g. covered calls) profit from Theta.

Vega (ν) — volatility sensitivity

Vega measures the price change for a 1% change in implied volatility (IV).

Example: a Vega of 0.20 means a 1% rise in IV adds about $0.20 to the option.

Higher Vega means more sensitivity to volatility. Options on volatile stocks, or heading into earnings, carry richer premiums.

Rho (ρ) — interest-rate sensitivity

Rho measures the price change for a 1% change in interest rates. Calls have positive Rho (higher rates help); puts have negative Rho.

Example: a Rho of 0.05 means a 1% rate rise adds about $0.05 to a call.

Rho barely matters for short-dated options but can move long-dated contracts.

Using the Greeks to manage risk

Put together, the Greeks tell you where your risk actually sits:

- Delta & Gamma — track price exposure and how it shifts as the stock moves.

- Theta — watch time decay if you're a short-term buyer; sellers can harvest it.

- Vega — adjust around volatility events like earnings, where high-Vega options swing hardest.

- Rho — factor it into long-dated positions when rates are moving.

Final thoughts

The Greeks give you a precise read on how each force pulls on an option's price. Together they turn risk from a vague worry into something you can measure and manage.

Next: basic options strategies — where all of this comes together in practice.

Educational content — not financial advice.